The Pros And Cons Of Blockchain You Should Know

In this post, we will discuss the pros and cons of blockchain technology, its advantages, and how it can benefit key sectors.

The blockchain has altered our perception of challenges. It has provided numerous benefits. Blockchain technology solves critical challenges such as network trust. By adjusting the main parameters, trust, every company can focus on tackling the problems at hand. Global governments have also recognized its significance and are eager to use blockchain technology. For example, Dubai Smart City 2020 is a project that intends to develop a smart city using emerging technologies such as blockchain.

The Pros And Cons Of Blockchain

Blockchain technology has been described as a disruptive technology that provides never-before-seen levels of security, which are required and wanted not only by the IT or finance industries but by any form of industry in general, making it an exceptionally flexible technology.

Despite its numerous advantages, Blockchain technology is far from flawless and, like any disruptive technology, has advantages and problems in its adoption. Let's have a look at some of them.

Pros of Blockchain

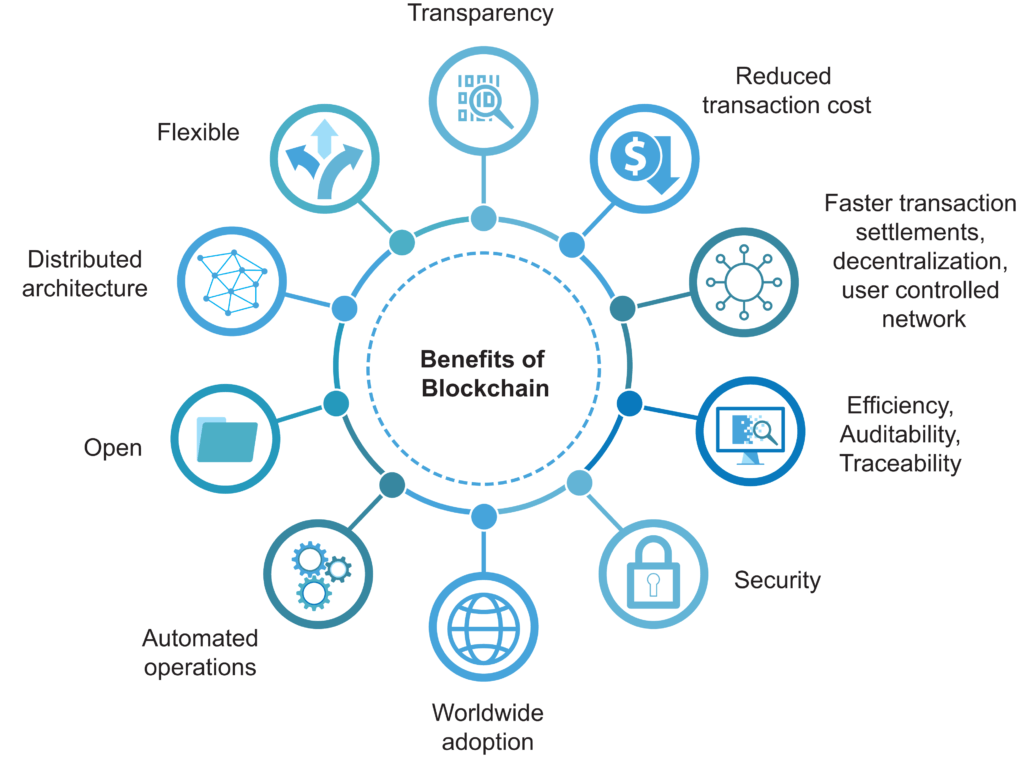

Better Transparency

Transparency is a major concern in today's industry. Organizations have attempted to introduce more rules and laws in order to promote openness. However, there is one factor that prevents any system from being completely transparent: centralization.

Increased Efficiency

Because of its decentralized nature, Blockchain eliminates the need for middlemen in many transactions, including payments and real estate. In comparison to traditional financial services, blockchain enables speedier transactions by enabling peer-to-peer cross-border payments using a digital currency. A uniform system of ownership data, as well as smart contracts that automate tenant-landlord agreements, make property management operations more efficient.

Enhanced Security

In comparison to previous platforms or record-keeping methods, blockchain technology employs greater security. Any transactions that are recorded must be agreed upon using the consensus technique. In addition, using a hashing algorithm, each transaction is encrypted and has a proper link to the previous transaction.

The fact that each node has a copy of every transaction ever conducted on the network adds another layer of security. As a result, if a malicious actor tries to modify the transaction, he will be unable to do so because other nodes will reject his request to write transactions to the network.

Blockchain networks are also immutable, which means that once data has been written, it cannot be reversed in any way.

Improved Traceability

With the blockchain ledger, an audit trail is present to trace where the items came from each time an exchange of goods is recorded on a Blockchain. This can help not only increase security and fraud prevention in exchange-related enterprises, but it can also help verify the legitimacy of exchanged assets. It can be used in businesses such as medicine to follow the supply chain from producer to distributor, or in the arts to provide indisputable proof of ownership.

Reduced Costs

Businesses are currently spending a lot of money to improve the management of their current system. That's why they seek to save costs and reinvest the savings in new projects or improvements to existing ones.

Organizations can save money by eliminating the need for third-party vendors by utilizing blockchain. There is no need to pay vendor fees because blockchain has no inherited centralized player. Furthermore, there is less engagement required while authenticating a transaction, minimizing the need to spend money or time on mundane tasks.

Advantages of Blockchain Technology

- Your business processes will be better safeguarded with blockchain thanks to its high level of security.

- Hacking threats to your company will also be decreased to a larger level.

- Because blockchain is a decentralized platform, there is no need to pay for the services of centralized corporations or middlemen.

- Enterprise blockchain technology enables businesses to use various levels of accessibility.

- With the support of blockchain, businesses can complete transactions more quickly.

- Account reconciliation is a process that can be automated.

- Transactions are transparent and thus easy to track.

Cons Of Blockchain

The Human Element

While it is important for all parties of a supply chain to understand that the data on the blockchain cannot be modified once it is established, there is still the possibility of human error or purposeful misbehavior in entering the initial data onto the blockchain. As a result, blockchain data is not perfect information - it may be incorrect or even fake. For example, a bad actor could fill a container with rocks but a record on the blockchain that it was full of auto parts. Blockchain technology may make it easier to determine where in the supply chain the container was filled with rocks, but it will not prevent fake data from reaching the blockchain in the first place. In essence, blockchain technology does not prohibit inaccurate information from being placed onto the chain; rather, it allows every user on the blockchain to validate that the data on the blockchain has not changed since a specific point in time. Because blockchain technology is typically unchangeable, false data added onto the chain is a source of concern. Accenture has created a prototype that will allow authorities of permissioned blockchains to edit previous transactions in exceptional circumstances to resolve human error1, though some blockchain technologists have criticized such approaches to blockchain, claiming that erasing immutability defeats the purpose of using blockchain over a traditional database.

Upfront Costs

The initial costs of adopting blockchain technology may be prohibitively expensive. Employing blockchain developers has costs, which tend to be higher than hiring regular developers due to their specialized field of knowledge. Planning fees, licensing fees, and maintenance fees can all add up to a heavy price tag.

Scalability Is An Issue

Blockchains are not as scalable as their centralized counterparts. If you've ever used the Bitcoin network, you'll know that transactions are processed based on network congestion. This issue is connected to blockchain network scalability issues. Simply put, the more individuals or nodes join the network, the more likely it will slow down!

However, there has been a significant shift in how blockchain technology operates. Scalability solutions are also being introduced into the Bitcoin network as the technology evolves. The solution is to conduct transactions outside of blockchain and solely utilize the blockchain to store and retrieve data.

Aside from that, there are new approaches to scalability, such as permissioned networks or employing a different architectural blockchain solution, such as Corda.

However, none of these methods are as effective as centralized systems. When comparing Bitcoin and VISA transaction speeds, you will notice a significant difference. Bitcoin now has a transaction rate of 4.6 transactions per second. VISA, on the other hand, can process 1700 transactions per second. This means that it can perform 150 million transactions per second in a single day.

Finally, we might state that blockchain may not be ready for real-world applications just yet. It still requires a lot of work before it can be used in everyday life.

Unemployment

Because there will be no need for intermediaries once Blockchain technology is embraced and implemented, all of these intermediation sectors for the validation of payments and procedures will inevitably be reduced to the point of disappearance, as would the jobs required for them.

Private keys

Excessive security can also be an Achilles heel; for example, in the case of private keys, as has been recorded numerous times, once lost, it is nearly hard to recover these keys, posing a concern for all holders of cryptographic values.

Conclusion

This brings us to the end of our discussion of the pros and cons of blockchain technology. Now that you understand the significance of blockchain technology, you can make an informed decision about whether or not to use it.

Blockchain is a game-changing technology that will have a significant impact on every industry. Our attention was limited to the most important industries so that you could relate to and appreciate their benefits.

But, in the end, the choice is totally yours. Hopefully, this advice will assist you in selecting the best selection for your company.